Starting November 2, 2026, homebuyers and homeowners will witness the most significant modernization of the home appraisal process in over a decade. This shift, driven by the implementation of Uniform Appraisal Dataset (UAD) 3.6, replaces legacy static forms with a dynamic, data-centric reporting system required by Fannie Mae and Freddie Mac. While the core methodology for determining a home's market value remains unchanged, the way that value is documented and reviewed is becoming far more precise.

For the average consumer, this means the "black box" of appraisal reporting is turning into a transparent, data-driven digital record. By moving away from subjective narrative comments and toward standardized data fields, the GSEs (Government-Sponsored Enterprises) aim to reduce human error, minimize bias, and accelerate the often-tedious underwriting process.

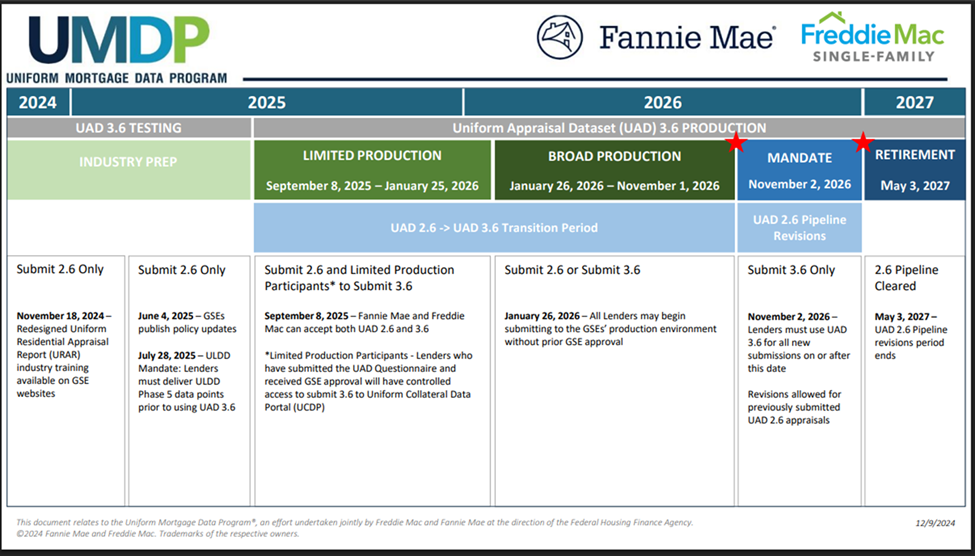

Why is the UAD 3.6 Redesign Happening Now?

The primary driver behind UAD 3.6 is the transition from static, paper-like PDF forms to a flexible, data-driven URAR (Uniform Residential Appraisal Report). Since 2005, the industry has relied on Form 1004, a rigid template that often forced appraisers to "fit" complex property data into small, restricted boxes.

The new standard aligns with MISMO 3.6 industry data protocols, allowing appraisal data to "talk" seamlessly to lender software and automated underwriting systems. According to industry analysis, this transition is currently in its "Broad Production" phase, which began in early 2026, giving the entire mortgage ecosystem a window to adapt before the mandatory deadline this November.

What Are the Key Changes in Local Appraisal Reports?

The most visible change for homeowners is the shift from "narrative" to "structured" data. In the past, an appraiser might write a short paragraph describing a "beautifully upgraded kitchen." Under UAD 3.6, that same kitchen is broken down into specific data points: cabinet materials, countertop types, appliance grades, and the exact year of the last renovation.

According to Fannie Mae’s 2026 Appraiser Update, specific granular adjustments include:

Range of View: Appraisers now categorize views as Full, Partial, or Seasonal, rather than just "Beneficial" or "Adverse."

Condition detail: Specific safety features and structural upgrades now have dedicated checkboxes and data fields rather than being buried in a 10-page addendum.

Dynamic Formatting: The report "grows" or "shrinks" based on the property. A single-family home with an accessory dwelling unit (ADU) will automatically include the necessary fields for that unit, rather than the appraiser having to attach separate, disparate forms.

How UAD 3.6 Benefits Homebuyers and Sellers

While UAD 3.6 is a technical reporting standard, its ripples affect the consumer experience directly. The goal is to move the mortgage industry toward "value acceptance" (formerly called appraisal waivers) and more consistent, reliable loan approvals.

For Homebuyers: Faster Closing Timelines

One of the leading causes of loan delays is "stipulations" or "stips"—requests from underwriters for an appraiser to clarify a comment or provide more detail on a specific property feature. Because UAD 3.6 uses integrated validation rules, the software flags missing or inconsistent data before the appraiser even hits "submit." This reduction in human error can trim days off the loan approval process, helping buyers hit their contractual closing dates.

For Homeowners and Sellers: Better Recognition of Upgrades

Under the old system, a high-end HVAC system or expensive solar array might be mentioned in the appraisal notes but not explicitly "weighted" in a way that was easy for a lender to see. The new structured format forces the report to highlight specific upgrades. This ensures that a well-documented kitchen remodel or energy-efficient window installation is captured as a distinct data point, making it harder to overlook when compared to other homes in the area.

Preparation Checklist: Helping Your Appraiser Under UAD 3.6

Because the new reporting format is so data-hungry, homeowners can significantly help their appraisal outcome by providing organized information upfront. The more "data" you provide, the less the appraiser has to search for, which leads to a more accurate report.

Feature Type | What to Document for UAD 3.6 | Why It Matters |

|---|---|---|

Major Systems | Exact age and model of HVAC, Water Heater, and Roof. | Allows for precise "remaining life" calculations in the report. |

Interior Remodels | Itemized list of materials (Quartz vs. Granite) and year of completion. | These are now specific data fields rather than general comments. |

Energy Efficiency | Solar panel lease/ownership terms and HERS ratings if available. | Structured data fields now exist for specific green features. |

Structural Repairs | Invoices for foundation work, basement waterproofing, or drainage. | Standardized fields require appraisers to note recent remediations. |

The Expert Tip for a Successful Inspection

Create a "House Resume." Before the appraiser walks through your front door, have a folder ready with a list of every major improvement made in the last 10 years, including the cost and the year completed. In the UAD 3.6 environment, having the exact year of an upgrade is much more valuable than saying it was done "a few years ago."

Common Myths About the 2026 Appraisal Standard

With any major regulatory shift, misconceptions often arise. It is important for homeowners to understand what UAD 3.6 does not do:

It does not change your home's value: The market determines value based on supply, demand, and comparable sales. This is simply a new way of writing the summary of those facts.

It does not replace the appraiser with an AI: While the reporting is more digital, a licensed professional appraiser still performs the physical inspection and applies expert judgment to select the best comparable properties.

It does not make appraisals more expensive: While appraisers have to learn new software, the technology is designed to make them more efficient. Most homeowners should not see a change in the appraisal fee charged by the lender.

The Bottom Line: Transparency for the 2026 Housing Market

UAD 3.6 is a massive leap forward in making the American mortgage process more modern and data-transparent. By replacing archaic forms with a single, flexible digital report, Fannie Mae and Freddie Mac are ensuring that home valuations are grounded in hard data rather than narrative interpretation.

Whether you are a buyer looking for a smoother path to homeownership or a seller wanting credit for every dollar spent on renovations, this new standard is designed to protect all parties by providing a clearer, more detailed picture of a property's true condition. As the November 2, 2026 mandate nears, staying informed and prepared with your property data is the best way to ensure your next real estate transaction is as seamless as possible.

Strengthening Market Stability Through Data Integrity

The shift to UAD 3.6 isn't just about faster paperwork; it's a structural reinforcement of the entire U.S. housing market. By collecting data in a more uniform way across millions of properties, Fannie Mae and Freddie Mac can better identify broad market trends and potential risks. For the individual homeowner, this industry-wide transparency helps ensure that your home’s value is being judged against the most accurate and comparable data available.

When appraisers use the standardized MISMO 3.6 language, it creates a digital "twin" of the property's condition and quality. This reduces the likelihood of "appraisal gaps"—where a lender's automated system disagrees with a human appraiser's manual report—because both are finally speaking the same technical language. This alignment is vital for maintaining the flow of credit and ensuring that mortgage interest rates remain competitive by reducing the operational risk for lenders.

Future-Proofing Your Home's Digital Financial Record

As we move deeper into 2026, the appraisal is evolving from a one-time document into a living financial record. Information captured under UAD 3.6 protocols will likely influence future digital evaluations and automated value models (AVMs). Homeowners who meticulously document their properties today are essentially "future-proofing" their home's digital profile.

If you plan to refinance or sell in the next five years, the data captured in a UAD 3.6 report this year will serve as the baseline for your next valuation. By ensuring every energy-efficient upgrade and structural improvement is logged in the GSEs' centralized database, you are protecting your equity and making your home more "market-ready" for the digital age of real estate. This level of detail provides a secondary layer of protection against market volatility, as a well-documented home is always easier to value accurately than one with a generic or outdated reporting history.

Discussion