Navigating the Hamilton County housing market as a first-time homebuyer requires more than just a pre-approval letter; it demands a strategic understanding of one of Indiana’s most competitive real estate landscapes. With 30-year mortgage rates averaging around 6.6% in mid-2026, buyers in Carmel, Fishers, and Noblesville must balance premium home prices against specific local tax structures and down payment incentives.

As a Senior Loan Officer at Fairway Independent Mortgage Corporation based in Carmel, I help families reconcile their long-term financial goals with the realities of our local market. This guide provides the data-driven clarity you need to move from browsing listings to signing a closing disclosure. Apply by clicking here.

2026 Hamilton County Home Prices by Township

Hamilton County continues to lead Indiana in home value appreciation, with median prices significantly higher than the state average. Entry-level homes in growing areas like northern Noblesville or Westfield typically begin in the $375,000 to $450,000 range, while established markets in Carmel and Fishers often see "starter" homes listed closer to $500,000.

For 2026, the Federal Housing Finance Agency (FHFA) has set the baseline conforming loan limit at $832,750 for single-family properties. This is a critical threshold for first-time buyers, as loans within this limit qualify for conventional financing terms from Fannie Mae and Freddie Mac. Homes exceeding this amount transition into "Jumbo" territory, which often carries stricter credit and reserve requirements.

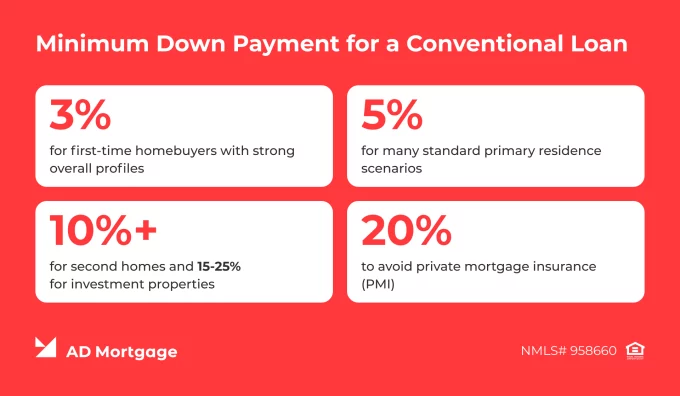

Lowering Upfront Costs: 2026 Down Payment Expectations

The "20% down" requirement is a common misconception that often prevents qualified buyers from entering the market. In reality, multiple loan programs allow for significantly lower entry points. According to research from Fannie Mae, qualified first-time buyers can often secure a mortgage with as little as 3% down on a conventional loan.

Here is a quick look at common down payment options available in Hamilton County:

Conventional (First-Time Buyer): 3% minimum down.

FHA Loans: 3.5% minimum down.

VA Loans: 0% down for eligible veterans and active-duty service members.

IHCDA Assistance: Programs like Next Home can bridge the gap for those with less than 3% saved.

While a lower down payment increases your monthly mortgage insurance (PMI) cost, it allows buyers to keep cash reserves for home maintenance or immediate improvements—a vital consideration given the competitive bidding environments we've seen throughout 2026.

Calculating Your All-In Monthly Mortgage Payment

Understanding your "all-in" monthly payment is more important than the purchase price alone. A monthly mortgage payment consists of Principal, Interest, Taxes, and Insurance (PITI). In Hamilton County, where property values are high, the tax and insurance portions of your payment are substantial.

Home Price | Down Payment (3%) | Loan Amount | Est. PI Payment (6.6%) |

|---|---|---|---|

$400,000 | $12,000 | $388,000 | $2,478 |

$500,000 | $15,000 | $485,000 | $3,097 |

$600,000 | $18,000 | $582,000 | $3,717 |

Note: These figures represent only Principal and Interest based on a *[6.6% MBA average rate](https://tradingeconomics.com/united-states/mortgage-rate). Taxes, insurance, and PMI would be added to these totals. For a $500,000 home, a realistic all-in payment would likely range from $3,800 to $4,100 per month depending on township tax rates. Accurate local estimation is essential to avoid second-year escrow shortages.*

2026 Hamilton County Property Tax Rates by District

Hamilton County homeowners benefit from Indiana's 1% homestead tax cap, but local school and safety referendums often push the effective rate higher. For 2026, certified data from the local auditor shows significant variation between our most popular school districts.

Typical effective tax rates (post-referendum) for 2026 include:

Carmel-Clay: Approximately 1.24%, which includes the 0.19% school operating referendum for one of the state's top-performing districts.

Fishers / HSE (Delaware Twp): Approximately 1.79% for city residents, reflecting the investments in the Fishers District and local infrastructure.

Westfield Washington: Approximately 1.96% in several newer developments, where growth assessments are highest.

Noblesville: Rates vary from 1.83% in the township to 2.70% within city limits for non-homestead properties (though the 1% cap still protects primary residents).

It is essential to understand that while the 1% cap limits the "base" tax, referendums for school safety and operations are exempt from that cap, which is why your actual bill may exceed $1 per $100 of assessed value. I recommend using a median effective rate of 1.10% as a conservative baseline for Carmel and Fishers budget planning until your specific parcel is certified. This ensures your mortgage escrow stays balanced.

Closing Costs: Budgeting for Your Final Transaction

Closing costs in Hamilton County usually range from 2% to 5% of the loan amount. These are the fees required to finalize the transaction and are paid at the time of closing, separate from your down payment. The Mortgage Bankers Association (MBA) forecasts a steady volume of originations through 2026, keeping these regional costs relatively stable.

Standard closing costs you will encounter in Indiana:

Lender Fees: Application, processing, and underwriting fees.

Third-Party Fees: Appraisal, credit report, and title insurance.

Prepaid Items: Escrow deposits for property taxes and homeowners insurance (usually 6–12 months of insurance plus several months of taxes).

County Fees: Recording fees for the deed and mortgage with the Hamilton County Recorder.

I always recommend that buyers request a Loan Estimate early in the process. This standard CFPB document allows you to see every fee in detail and ensures there are no surprises when you arrive at the title company in Carmel or Fishers.

Summary Checklist for Hamilton County Buyers

To succeed in this market, timing and preparation are everything. Follow these four steps to position yourself for a successful purchase:

Verify your budget with a local lender who understands Hamilton County township taxes and homestead deductions.

Review the local price floor. Expect "entry-level" to sit between $375k–$450k for move-in ready homes.

Plan for both down payment and closing costs. Total cash to close is often 5%–8% of the purchase price when combined.

Monitor conforming limits. Keep your search within the $832,750 baseline to maximize your financing options.

Hamilton County remains one of the best places in the Midwest to invest in homeownership. By entering the market with a clear financial roadmap, you can secure a home that serves as both a sanctuary and a sound financial foundation.

Which mortgage loan types are best for Indiana buyers?

Choosing the right financing structure is as critical as finding the right home. While many buyers equate a mortgage with a standard 30-year conventional loan, the local market in Hamilton County offers several specialized paths—some of which are designed specifically to mitigate the higher entry costs of our suburbs.

Conventional Financing

The most versatile option for those with stable credit. For 2026, many lenders offer "Conventional 1% Down" programs or specific state-level grants that pair with Fannie Mae’s HomeReady or Freddie Mac’s Home Possible initiatives. These are ideal for the modern professional in Fishers or Carmel who has high income but has not yet built a massive savings cushion.

FHA Loans (Federal Housing Administration)

FHA loans remain a cornerstone for buyers who may have lower credit scores (often down to 580) or higher debt-to-income ratios. Because Hamilton County homes are at a higher price point, ensure your target home falls within the local FHA loan limits, which generally track with conforming limits but can vary by county.

VA Loans (Veterans Affairs)

For our veterans in Hamilton County, VA loans are arguably the most powerful wealth-building tool available. They require $0 down payment and carry no monthly mortgage insurance, which can save a buyer $200–$400 per month compared to a conventional loan on a $500,000 home.

Your Next Steps: From Selection to Signature

Hamilton County remains one of the best places in the Midwest to invest in homeownership. By entering the market with a clear financial roadmap—pairing high-tier township tax data with the right down payment assistance—you can secure a home that serves as both a sanctuary and a sound financial foundation.

To move from browsing Zillow to holding your new keys in Carmel, Fishers, or Westfield, your focus must remain on preparation. Contact a local Hamilton County mortgage expert today to lock in your 2026 strategy, verify your IHCDA eligibility, and receive a customized Loan Estimate for your target neighborhood. Let's make your first home a reality.

IHCDA Down Payment Assistance Programs

State-sponsored programs can significantly lower your upfront cash requirements when purchasing a suburban home. In 2026, the Indiana Housing and Community Development Authority (IHCDA) provides a couple of targeted options that pair with major mortgage structures to offset down payment and closing costs.

Next Home Program: This initiative provides matching funds of up to 3.5% of the purchase price to cover your down payment. Unlike standard grant programs, Next Home does not carry a strict first-time buyer restriction, making it highly flexible for growing families shifting into larger Hamilton County school districts.

First Step Program: Exclusively designed for first-time buyers, this program offers a larger buffer of 5% of the property purchase price in down payment assistance. Eligibility centers on local income limits and credit score baselines, typically requiring a 660 minimum credit score to participate.

Both programs must be executed through an IHCDA-approved participating lender. Because Hamilton County features a higher median home valuation than surrounding areas, ensuring your household income complies with local area median income (AMI) limits is a vital initial step before underwriting begins.

How do you win a bidding war in a high-demand market?

In 2026, "winning" a home in Hamilton County often requires more than just the highest price; it requires a contract that minimizes risk for the seller. According to the Mortgage Bankers Association (MBA) 2026 outlook, demand in high-tier markets like ours is expected to remain firm even as inventory fluctuates.

The Power of Local Pre-Approval

A pre-approval from a local Hamilton County lender carries significant weight with local listing agents. When an agent in Noblesville sees a Fairway header on a pre-approval, they know the local taxes have been calculated correctly and the appraisal will be handled by someone familiar with our specific neighborhoods.

Shortening the Appraisal Gap

Given the rapid appreciation in areas like Westfield, some buyers choose to include an "appraisal gap guarantee." This clause states that if the home appraises lower than the offer price, the buyer will cover a specific portion of the difference in cash. This is a high-level strategy that should only be executed after a deep dive into your available liquid reserves.

Inspection Strategies

While we never recommend waiving an inspection entirely, modern buyers often use an "As-Is with Right to Terminate" clause. This tells the seller you won't nickel-and-dime them for small repairs, but you still have the protection to walk away if a major foundation or roof issue is discovered.

Why is a "Local Tax Expert" necessary for your mortgage?

One of the biggest mistakes a first-time buyer can make is using a national "big box" online lender that doesn't understand Indiana’s unique property tax system. In any mortgage calculation, "T" (Taxes) is a variable that can swing your monthly payment by hundreds of dollars.

As of 2026 data from the DLGF, tax rates in Hamilton County are highly township-dependent. If a lender from California or New York estimates your taxes based on a national average of 1.2%, but you buy a home in a specific pocket of Fishers where the effective rate—after school referendums—is closer to 0.9%, your pre-approval could be significantly off-base. Worse, if they underestimate your taxes, you could face a massive "escrow shortage" bill twelve months after you move in.

My role is to ensure your "Cash to Close" and "Monthly Payment" are as accurate on day one as they are on the day you sign. We look at the specific homestead impacts for each township and cross-reference them with actual MIBOR listing data to ensure you aren't surprised by an "assessment catch-up" in your second year of homeownership.

Frequently Asked Questions

Can I buy a home in Hamilton County with a credit score below 620?

Yes. Both FHA and VA programs allow for scores below 620, though you may face slightly higher interest rates or require a larger down payment in some cases. However, for a $400k+ purchase, bringing your score above 680 will significantly improve your conventional loan options.

What is a "referendum tax" and why is it on my bill?

Many Hamilton County school districts (like Noblesville or Westfield-Washington) have passed voter-approved referendums to fund teacher salaries and facilities. These are added to your property tax bill. While they increase the payment slightly, they are a primary reason why Hamilton County property values remain so resilient.

Is homeowners insurance higher in Indiana than other states?

Indiana is generally considered affordable for insurance, but because we are in a high-wind and hail region, it is more expensive than some western states. Expect to budget between $1,200 and $2,200 annually for a typical $500,000 home.

How do I apply for my Homestead Deduction?

You generally apply through the Hamilton County Auditor's office after you have closed and moved into the home. It is not automatic. Most buyers must file by December 31st of the year they buy to see the tax savings in the following year's bill.

Discussion