The Florida real estate market in 2026 presents a dual-edged opportunity: while statewide inventory has grown nearly 10% and median prices have stabilized, rising insurance costs and shifting tax laws require a sophisticated entry strategy. Success in this landscape is no longer about simple appreciation; it is about local yield optimization and navigating the legislative pivot points scheduled for 2027.

Buying an investment property here requires mastering three specific domains: the financing shift toward debt-service coverage ratio (DSCR) loans, the impact of the upcoming 2026 property tax ballot, and the hyper-local divergence between stabilizing metros like Palm Beach and softer markets in the Florida Panhandle.

Expert Insight: "In 2026, the Florida market rewards precision over speculation. Success is found in the 'amenity gap' and proactive insurance mitigation," says Loodmy Jacques, a leading REALTOR with KW Reserve Palm Beach. With years of experience navigating the West Palm Beach market, Loodmy specializes in helping investors identify high-yield opportunities in Florida's shifting regulatory landscape.

Florida remains a high-yielding environment because of its persistent net migration and a tightening supply of new listings, which fell 1.8% in mid-2026. This constricted "new supply" pipeline often supports rental floors even when sales volume fluctuates.

The state's median sold price is roughly $395,000 as of mid-2026, representing a modest 1.7% year-over-year increase. However, the average sale price in high-demand pockets like Palm Beach County has surged past $1 million, driven by the luxury segment. For investors, this means the "middle-market" ($500,000–$750,000) is the most competitive, often entering seller's market territory despite the broader statewide stabilization.

How Do You Finance a Florida Investment Property?

Financing for non-owner-occupied properties in 2026 typically requires a 20% to 25% down payment and interest rates roughly 0.5% to 1.0% higher than primary residential mortgages. In a high-rate environment, traditional income verification (W-2) is increasingly being bypassed for specialized investor products.

Many professional investors now utilize DSCR loans, which qualify the borrower based on the property’s rental income rather than personal debt-to-income ratios.

Loan Type | Typical Down Payment | Key Requirement | Best For |

|---|---|---|---|

Conventional Investment | 15%–25% | Strong DTI & 620+ Credit | Long-term holds with verified personal income |

DSCR Loan | 20%–30% | Rental income > Mortgage (PITI) | Scaling a portfolio without DTI constraints |

Hard Money | 10%–20% | ARV (After Repair Value) Focus | Fix-and-flip or major renovations |

Owner-Occupied (House Hack) | 0%–3.5% | Must live on-site 1 year | Entry-level investors buying 2–4 unit properties |

Florida Property Tax Caps and Insurance Cost Mitigation

The most critical factor for 2026 buyers is Amendment 3, a ballot measure that could eliminate homestead property taxes for many residents by 2027. While this primarily benefits owners, it carries a vital provision for investors: it proposes lowering the annual assessment cap on non-homestead properties from 10% to 5%).

Analyzing the Real-World Impact of Insurance Premiums

Insurance remains the primary "expense leak" for Florida landlords. To illustrate the impact, consider a median-priced home valued at $395,000. Based on the 1.5% to 2.5% budgeting rule:

Low-End Estimate (1.5%): A well-mitigated inland home would cost approximately $5,925 per year ($493/month).

High-End Estimate (2.5%): A premium coastal property or one lacking modern wind mitigation could reach $9,875 per year ($823/month).

This $330 monthly difference is often the deciding factor in whether a property achieves a positive cash-on-cash return. Investors should prioritize "Zone X" locations and impact-rated upgrades to stay on the lower end of this spectrum.

Best Cities for Florida Rental Yields in 2026

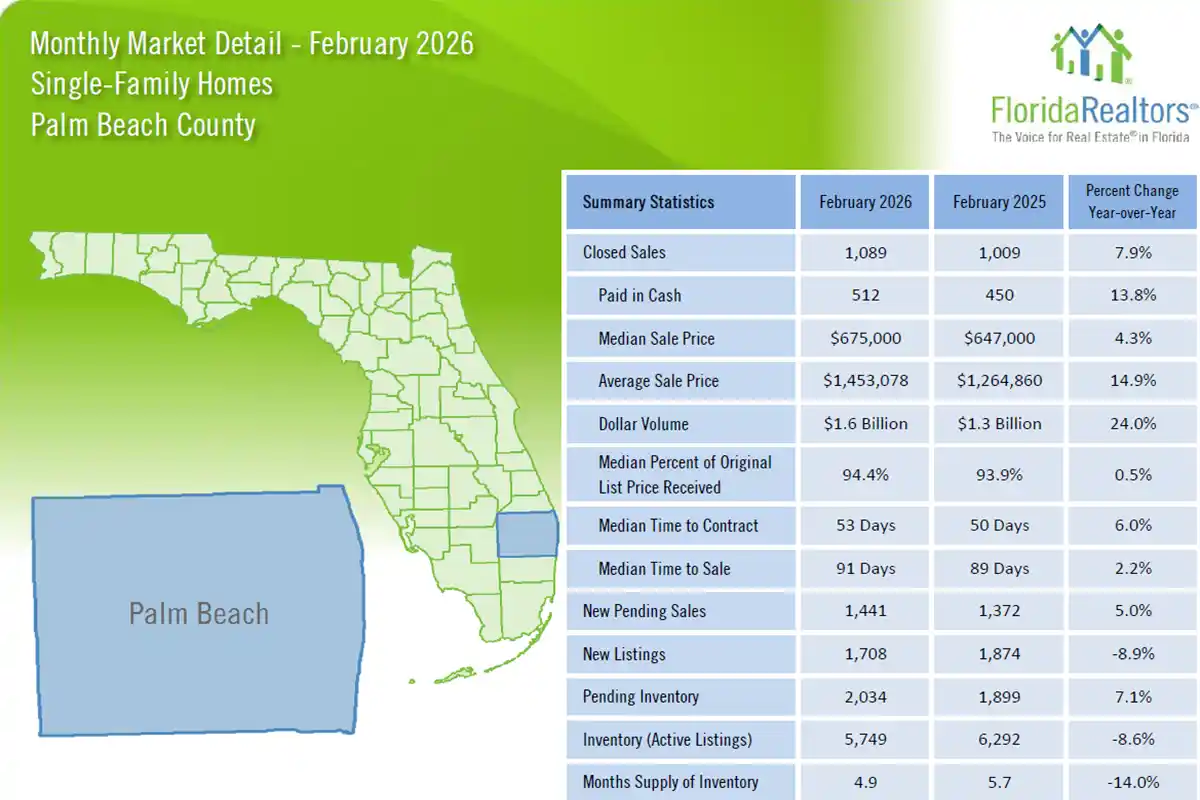

Stabilization is the 2026 theme for Florida's major metros. While South Florida experienced a "softness" in median prices in Broward County (down 1%), Palm Beach County showed strong growth with an 11% jump in average sale prices.

Why West Palm Beach is the Top Choice for Luxury Yields

West Palm Beach has become a high-end rental market fueled by the "Wall Street South" migration. High-income professionals are seeking luxury condos and modern single-family homes, driving rent appreciation in the downtown core.

Short-Term Rental Potential in Orlando and Kissimmee

These markets remain dominant for short-term vacation rentals, though regulatory oversight on Airbnbs has increased 20% since 2024. Investors here must focus on high-amenity properties to stand out in a crowded market.

Balanced Growth in Tampa and St. Petersburg

The Tampa Bay area offers a balanced mix of 10% inventory growth and robust year-round corporate demand, making it a "safe haven" for long-term buy-and-hold strategies.

Understanding the "Wall Street South" Expansion

The phrase "Wall Street South" has transitioned from a marketing buzzword to a physical reality that fundamentally alters West Palm Beach investment mathematics. In 2026, the concentration of financial services firms moving from New York and Connecticut into downtown West Palm Beach has reached a critical mass, creating a high-income renter demographic that priorities luxury amenities over square footage.

This shift has created a unique opportunity in the "Class B" renovation space. Investors who acquire dated 1970s and 80s structures within a 3-mile radius of the financial district and perform high-end aesthetic upgrades are seeing rent premiums of up to 45% compared to non-renovated counterparts. The key is in the "amenity gap": these renters expect the same white-glove security, high-speed connectivity, and modern finishes they left behind in Manhattan.

The Impact of Commercial Infrastructure on Residential Yield

When evaluating a Florida property, the proximity to new commercial developments acts as a hedge against market volatility. In these corridors, land value appreciation has outpaced the general residential market by an average of 4.2% over the last 24 months. For an investor, this means your "exit strategy" is diversified: you can sell to another residential landlord or, in some cases, to developers looking for larger project assemblages.

Risk Management: The 2026 Insurance Crisis and Mitigations

It is impossible to discuss Florida investment without addressing the state's hard insurance market. By July 2026, while some legislative reforms from 2023 have finally reduced litigation volume, the primary drivers of cost—replacement value and reinsurance—remain high.

Pro-active Mitigation Strategies: Investors who want to maintain a high "Cap Rate" must prioritize properties with the following features:

Impact-Rated Windows: Not only do these lower your wind premium, but they also increase attractiveness to high-end tenants by reducing noise and improving energy efficiency.

Secondary Water Resistance (SWR): Ensuring a roof has an SWR layer can reduce insurance costs by nearly 15%.

Flood Zone Positioning: Avoid "Zone AE" if your goal is cash flow. The mandatory flood insurance premiums in these zones can consume up to 12% of your gross annual revenue, making "Zone X" properties significantly more profitable on a net basis.

The 2026 "Silver Tsunami": Senior Housing and Infill

Beyond traditional single-family rentals, 2026 is seeing a surge in demand for accessory dwelling units (ADUs). Florida’s aging population, combined with high housing costs for caregivers, has created a massive shortage of "infill" housing.

If you buy a property in a municipality that has relaxed its ADU laws (like parts of Hillsborough), you are essentially getting "two units for the price of one" and a half. Converting a detached garage into a studio apartment can increase your yield by 3.5% while only adding roughly 15% to your acquisition and renovation cost. This "secondary unit" strategy is one of the most effective ways to combat high interest rates, as it allows you to cross-subsidize the mortgage of the main house.

Navigating the "Non-Warrantable" Condo Trap

For many entry-level investors, Florida condos look attractive because of their lower entry price. However, in 2026, many condo associations have failed to meet the rigorous new structural reserve requirements mandated by post-Surfside legislation.

If an association has not fully funded its reserves, the condo becomes "non-warrantable," meaning Fannie Mae and Freddie Mac will not back the mortgage. This forces you into specialized portfolio loans or cash deals. Always demand a "Reserve Study" and the "Structural Integrity Reserve Study" (SIRS) before signing a contract. A low HOA fee today could turn into a $50,000 "special assessment" tomorrow.

The Legislative Pipeline: What Investors Need to Prepare For in 2027

Investing in 2026 means looking around the corner at the 2027 legislative session. There is currently significant momentum in Tallahassee to address the "Short-Term Rental Preemption" bill, which would standardize STR rules across the state.

What this means for you: If you currently own a property in a city with "hostile" STR laws, 2027 might be the year those laws are overturned by the state. Conversely, if you are in a "friendly" zone, you might see an influx of competition if the state levels the playing field. Buying now in an area with high "long-term demand" ensures that even if STR profitability fluctuates due to new supply, your floor remains secure.

2026 Investment Outlook: Strategy and Next Steps

The Florida market of 2026 is no longer a "timing market"; it is a "selection market." The difference between a 10% cash-on-cash return and a negative cash flow is the quality of your local team—from your REALTOR who understands the specific neighborhood dynamics to your insurance broker who has access to surplus lines that others don't.

Summary of the 2026 Real Estate Landscape

As we move into the second half of 2026, the data confirms that Florida remains a premier destination for capital preservation and long-term yield. The combination of Amendment 3's potential tax relief and the continued influx of high-wealth residents from the Northeast creates a floor for property values that many other states lack.

Your 2026 Investor Checklist

If you are ready to take the next step, focus on the "off-market" potential. In 2026, many older landlords who have held properties for 20+ years are looking to exit rather than deal with new insurance complexities.

Verify Your Financing: Get pre-approved for a DSCR loan if you plan to scale.

Order a Wind Mitigation Report: Do this early in the due diligence period to get accurate insurance quotes.

Contact a Global Specialist: Reach out to a local expert who understands both the "Wall Street South" luxury shift and the suburban infill demand.

Ready to start your Florida investment journey? Connect with Loodmy Jacques at KW Reserve Palm Beach to receive a curated list of high-yield properties currently entering the 2026 market.

Steps to Buying Your Florida Investment Property

Analyze the "Net" Yield: Do not look at gross rent. Subtract property taxes (budget 1.8%–2% of purchase price), insurance (budget for wind/flood), and a 10% property management fee.

Verify Rental Regulations: Many Florida municipalities (like Boca Raton or parts of Miami Beach) have strict "minimum stay" requirements. If you intend to do short-term rentals, check the city ordinance first.

Secure a Pre-Approval for Investors: Ensure your lender understands Florida’s unique condo-hotel or non-warrantable condo rules if you are looking at beachfront units.

Inspect for Mitigation: In 2026, a "Wind Mitigation" report is not optional—it is your best tool for reducing insurance premiums by up to 30%.

Audit the Tax History: Florida property taxes reset upon sale. Do not look at the seller's current tax bill; use a tax estimator based on the new purchase price.

Frequently Asked Questions

Can I buy a Florida investment property with 10% down?

Generally, no. For non-owner-occupied residential property, most lenders require at least 15%–20% down. The only way to put 10% down or less is through a second-home loan (which has strict usage restrictions) or by "house hacking" a multi-unit property as your primary residence.

How does the 2026 "Homestead" vote affect investors?

While investors don't get the homestead exemption, Amendment 3 includes a provision to slash the assessment cap in half) for rental and commercial properties. If passed in November 2026, your assessed value for tax purposes cannot grow more than 5% per year, providing significant long-term cost stability.

Is Airbnb or Long-Term Rental better in 2026?

Long-term rentals currently offer more stability as the "short-term rental gold rush" has led to increased supply and lower average daily rates (ADRs) in oversaturated markets. However, high-barrier-to-entry coastal markets still see superior returns on short-term rentals if the property has unique amenities like a private pool or beach access.

Discussion