The mortgage landscape is undergoing its most significant structural shift in decades, and it’s good news for home buyers. As of July 1, 2026, Fannie Mae and Freddie Mac have officially published historical data and implemented policies that allow lenders to use VantageScore 4.0 for government-backed loans. This move effectively ends the era where a single, traditional credit score determined who could own a home and who was left on the sidelines.

For years, the "Classic FICO" model was the undisputed gatekeeper of the American Dream. However, its rigid requirements often penalized "thin-file" borrowers—those with limited credit history but responsible financial habits. The transition to VantageScore 4.0 is not just a technical update; it is an expansion of credit access. By utilizing trended data and machine learning, this model allows lenders to see a more complete picture of a borrower’s reliability, potentially qualifying millions who were previously unscoreable.

3 Key Takeaways for Austin Buyers

Expanded Eligibility: The shift help scores approximately 37 million more consumers, particularly those with "thin" credit files.

Trended Data Matters: Lenders now look at your 24-month payment trajectory rather than just a single snapshot, rewarding consistent debt reduction.

Alternative Credit: For the first time, on-time rent and utility payments can be factored directly into your mortgage credit score.

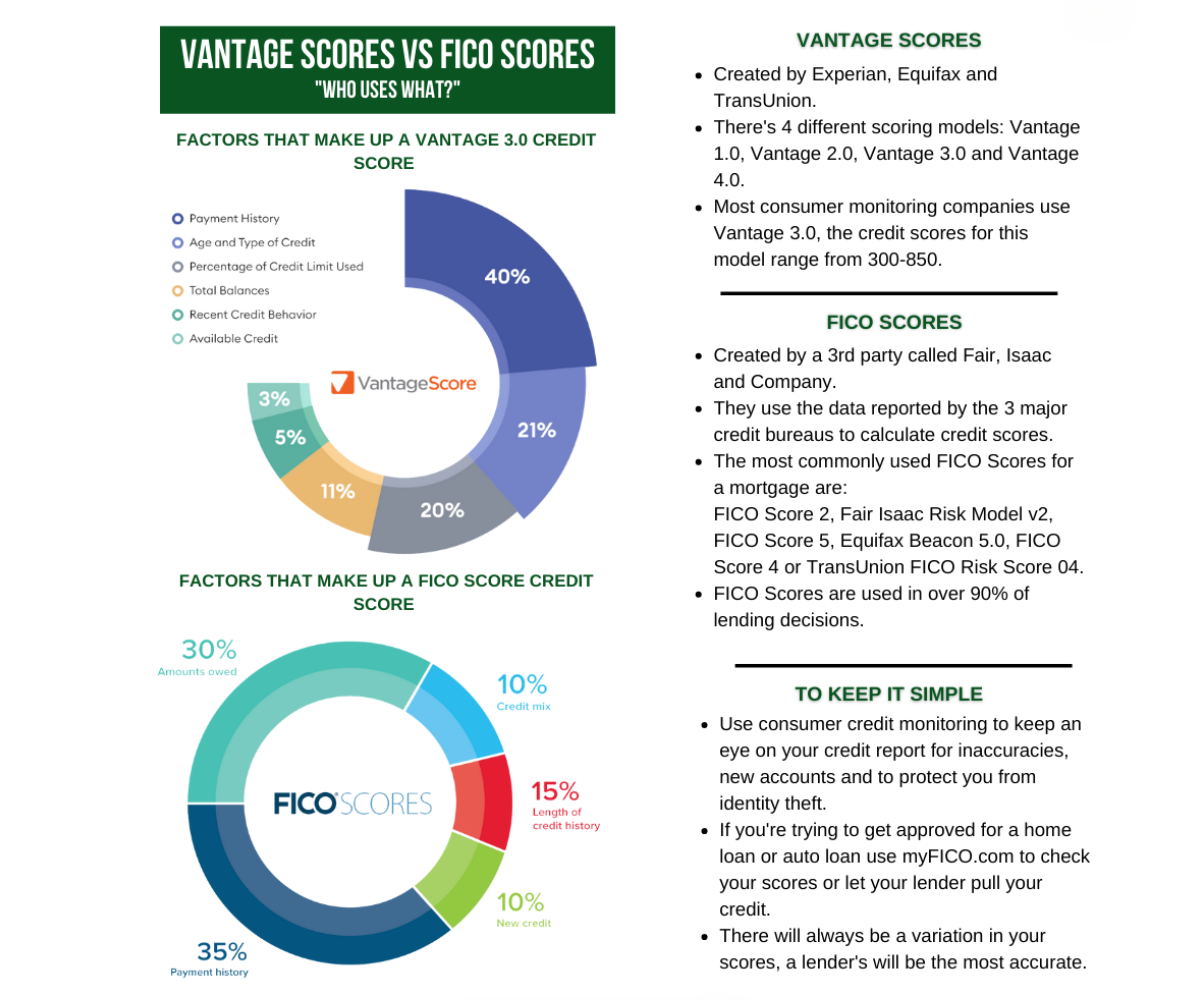

What is VantageScore 4.0?

VantageScore 4.0 is the first tri-bureau credit scoring model to incorporate trended credit data into its calculation, providing a dynamic look at a consumer’s financial behavior over time. While older models look at credit usage as a single snapshot in time, VantageScore 4.0 analyzes whether a borrower is "trajectory-positive"—meaning they are consistently paying down debt rather than just maintaining a balance.

The 30 largest mortgage originators in the U.S. have already integrated VantageScore 4.0 into their systems, signaling a massive industry-wide pivot. For borrowers, this means your score might finally reflect the reality of your financial life. Instead of being "punished" for a high balance one month, the model looks at your last 24 months of activity to determine your true risk level.

The Technical Frontier: Trended Data vs. Static Snapshots

To understand why VantageScore 4.0 is such a significant departure from the past, you have to look at how credit risk has traditionally been calculated. Legacy models operated like a high-speed camera: they took a single picture of your debt at a moment in time. If that photo was taken the day after you put a large wedding expense or a car repair on your credit card, you looked like a high-risk borrower, even if you paid the balance off in full 48 hours later.

VantageScore 4.0 operates more like a high-definition video. By analyzing 24 months of trended data, the model can identify the direction of your financial health. This is particularly vital in the 2026 economic environment, where inflation and fluctuating interest rates have forced many households to be more strategic with their cash flow.

A "trajectory-positive" borrower—someone whose debt levels are trending downward or whose revolving credit utilization is consistently low—receives a higher score than a "revolver" who maintains high balances month-to-month. This nuanced view allows lenders to feel more confident in borrowers who might have a high debt-to-income ratio on paper but show a clear history of disciplined repayment.

Bridging the Homeownership Gap for Marginalized Communities

One of the most profound impacts of the VantageScore 4.0 rollout is its potential to address historical disparities in homeownership. Statistics from May 2026 data indicate that minority and Gen Z populations are disproportionately represented among "thin-file" or "unscoreable" consumers.

Traditional credit scoring models often required a 12-to-24-month history of credit card or loan usage to generate a score. This effectively locked out:

Younger buyers (Gen Z): Who may prefer debit cards and "Buy Now, Pay Later" (BNPL) services over traditional credit cards.

Immigrant communities: Who may have significant income but lack a long-established history with U.S. credit bureaus.

Rent-first households: Individuals whose years of rent payments received zero "credit" in traditional FICO windows.

By incorporating machine learning and alternative data, VantageScore 4.0 effectively builds a bridge. If a buyer has a history of on-time rent and utility payments, the model can now translate that responsibility into a numeric score. This doesn't mean credit standards are being lowered; rather, the definition of "creditworthy" is being expanded to include modern financial behaviors.

The Economic Impact of Competition in Scoring

For nearly 20 years, the mortgage industry's reliance on a single proprietary score created a monopoly that many experts argue stifled innovation. The July 2026 transition has introduced much-needed competition to the secondary market.

When multiple models compete for a lender’s business, the borrower wins in several ways:

Pricing Transparency: The cost of a credit pull has dropped significantly for lenders using newer models, saving borrowers on upfront costs.

Product Innovation: Competition drives legacy providers to innovate faster, leading to a broader suite of tools for assessing risk.

Accuracy and Resilience: Even with macro headwinds, the average VantageScore increased to 701 in early 2026, reflecting the success of borrowers adapting to higher rates.

For a mortgage professional, these changes mean fewer "declined" notifications and more "pre-approved" conversations. We can finally look at a buyer who has been responsibly managing their finances outside of the legacy credit card ecosystem and find a viable path to homeownership.

Why does VantageScore 4.0 help more buyers qualify?

The primary reason VantageScore 4.0 is a game-changer is its ability to score roughly 37 million more consumers than legacy models. It does this by leveraging alternative data sources and relaxing the strict "activity" requirements found in traditional FICO models.

In the legacy system, if you hadn't used credit in six months, your score could vanish. VantageScore 4.0 changes that math.

Alternative Data Integration: It can factor in rent payments, utility bills, and telecom data if reported, which provides a path to credit for those who don't rely on traditional credit cards.

Trended Data Analysis: By looking at payment patterns over 24 months, the model can distinguish between a borrower who is spiraling into debt and one who is strategically managing a temporary balance.

Predictive Accuracy: VantageScore reports a 5.3% predictive lift in mortgage originations, meaning lenders can approve more loans without increasing their risk profile.

How is the FHFA implementing this change?

The Federal Housing Finance Agency (FHFA) has mandated a multi-year transition to modernize credit scoring. In April 2026, the Government-Sponsored Enterprises (GSEs)—Fannie Mae and Freddie Mac—formally updated their selling guides to include both VantageScore 4.0 and FICO 10T as approved models.

Currently, we are in a "competition phase" where lenders can choose to use VantageScore 4.0 or the Classic FICO model. This competition is already driving costs down for consumers. In early 2026, Equifax and TransUnion announced they would price [VantageScore 4.0 at $4.00 to $4.50 per score](https://newsroom.transunion.com/transunions-2026-mortgage-pricing-goes-live--prioritizing-lower-costs-for-homebuyers)—a significant discount compared to the roughly $10 price point for traditional FICO scores.

What do home buyers need to know now?

If you are planning to buy a home in 2026 or 2027, the first step is to check which model your lender is using. While the top 30 originators have adopted the new model, some local banks and smaller credit unions may still be in the process of updating their systems.

Key action items for buyers:

Ensure your rent is being reported: Since VantageScore 4.0 can factor in rental history, use services that report your on-time rent payments to the bureaus.

Focus on payment trajectory: It is no longer just about the current balance; it's about the trend. Aim to pay even slightly more than the minimum each month to show a downward trend in debt.

Check all three bureaus: Because VantageScore 4.0 is a tri-bureau model, consistency across Equifax, Experian, and TransUnion is more important than ever.

Is this the end of the FICO score?

No, but it is the end of the FICO monopoly. The industry is moving toward a "bi-merge" or "tri-merge" environment where multiple scores are considered. While FICO 10T is also being introduced, VantageScore 4.0 has gained a significant early lead in adoption due to its focus on financial inclusion and its aggressive pricing strategy in 2026.

This shift toward competition is designed to make the mortgage process more equitable. For the first time, the "gatekeeper" of homeownership isn't just one company’s algorithm, but a competitive marketplace that rewards lenders who find innovative ways to identify creditworthy buyers.

Frequently Asked Questions

Does every lender have to use VantageScore 4.0?

While Fannie Mae and Freddie Mac have approved the model, individual lenders still have the discretion to use VantageScore 4.0 or Classic FICO during the current transition period. However, most major national lenders have already switched to benefit from the increased accuracy and lower costs.

Will my VantageScore be higher than my FICO score?

Not necessarily, but it will be based on more data. If you have a "thin" credit file or a positive trend of paying down debt, your VantageScore 4.0 may be significantly more favorable than a traditional FICO score that only looks at a recent snapshot.

How do I get my VantageScore 4.0?

Most major banking apps and free credit monitoring services now provide VantageScore 3.0 or 4.0. To ensure you are seeing the 4.0 model specifically, you can check through the credit bureaus directly or ask your mortgage loan originator for a "dual-score" comparison during your pre-approval process.

Get Personalised Guidance on Your Mortgage Credit

Navigating the transition to VantageScore 4.0 can be complex, especially if you are working with a thin credit file or looking to optimize your "trajectory-positive" data before applying for a loan. As a mortgage professional based in Austin, TX, I help buyers understand how these scoring changes impact their specific financial profiles for successful home financing in Texas.

If you have questions about how your rent reporting or debt trends will be viewed by lenders in 2026, let's talk. You can learn more about my background at Matt.Mortgage or connect with me via a direct consultation.

Pro Tip: Schedule a 15-Minute Consultation Ready to see how your specific credit profile aligns with the new 2026 standards? Click here to book a 15-minute VantageScore consultation to review the differences between your "free app" score and the models used by Fannie Mae and Freddie Mac today.

Discussion