For many retirees in 2026, the equity in their home is not just a financial asset; it is a psychological fortress. Despite the availability of financial instruments like the Home Equity Conversion Mortgage (HECM), a significant segment of the senior population remains deeply resistant to tapping into their home’s value. This hesitance is often not a result of modern financial analysis, but rather a deeply ingrained set of values inherited from the cultural trauma of the Great Depression.

Understanding the resistance to reverse mortgages requires looking past contemporary interest rates and mortgage insurance premiums. It requires an exploration of the "Depression shadow"—a lingering fear of debt and a drive for total home ownership that has been passed down through generations.

How did the Great Depression shape senior attitudes toward home equity?

The Great Depression (1929–1939) fundamentally rewired the American psyche regarding debt and housing security. During this decade, unemployment reached 25% and approximately one-third of U.S. farmers lost their land to foreclosure. For the generation that lived through it, and the children they raised, the home became the only reliable safety net in an unpredictable world.

This historical period fostered a "scarcity mindset" that persists today. To many seniors, a mortgage—any mortgage—is viewed as a threat to their survival rather than a tool for liquidity. The psychological toll was so severe that jobless men often felt they lost primary decision-making power, leading to a lifelong obsession with maintaining a debt-free status as a marker of safety and dignity.

Why do seniors view home equity as a "legacy" rather than an asset?

For many older homeowners, the house is not a bank account; it is proof of their life's work and the primary vehicle for an intergenerational wealth transfer. Research indicates a significant relationship between giving financial transfers and the mental health of the giver. Seniors often feel a profound obligation to pass on a debt-free home to their children, viewing a reverse mortgage as "spending their children's inheritance."

This desire for a legacy often clashes with the reality of modern retirement costs. While a reverse mortgage could alleviate current financial stress, the perceived moral failure of leaving a smaller inheritance often outweighs the practical benefit of a more comfortable lifestyle. This intergenerational pressure is a direct descendant of the Depression-era belief that land and property are the only truly stable forms of wealth.

Why does the "debt-free" mantra feel like a moral obligation?

For the Silent Generation and older Baby Boomers, paying off a mortgage was once celebrated as the ultimate milestone of adulthood. This "burn the mortgage" culture was a direct response to the massive homelessness and bank runs of the 1930s. When a senior says they don't want a reverse mortgage, they aren't just rejecting a financial product; they are defending their identity as a "responsible" provider who has conquered the threat of debt.

In many immigrant and working-class communities, the home is also the only tangible proof of upward mobility across generations. To borrow against it feels like a reversal of progress. This emotional weight is often overlooked by financial advisors who focus solely on mathematical advantages. For these homeowners, the safety of a $0.00 balance is worth more than the utility of $100,000 in liquid cash, even if that cash could significantly improve their daily health and comfort.

How has the 2008 housing crisis reinforced Depression-era fears?

While the Great Depression set the foundation for home equity skepticism, the 2008 Great Recession served as a powerful "booster shot" for those fears. Many of today’s retirees watched their younger peers or neighbors lose homes to predatory lending and adjustable-rate mortgages during the mid-2000s. This more recent trauma reinforced the belief that banks are predatory entities and that any complex loan product is a "trap" designed to strip away equity.

Current market volatility in 2026 further complicates this perception. Seniors living on fixed incomes are naturally risk-averse, and the non-traditional structure of a reverse mortgage—where the debt grows rather than shrinks—feels intuitively dangerous to someone who equates debt growth with financial ruin. To overcome this, the industry must pivot toward transparency, emphasizing that modern HECMs have federal protections that did not exist during the eras of historical crashes.

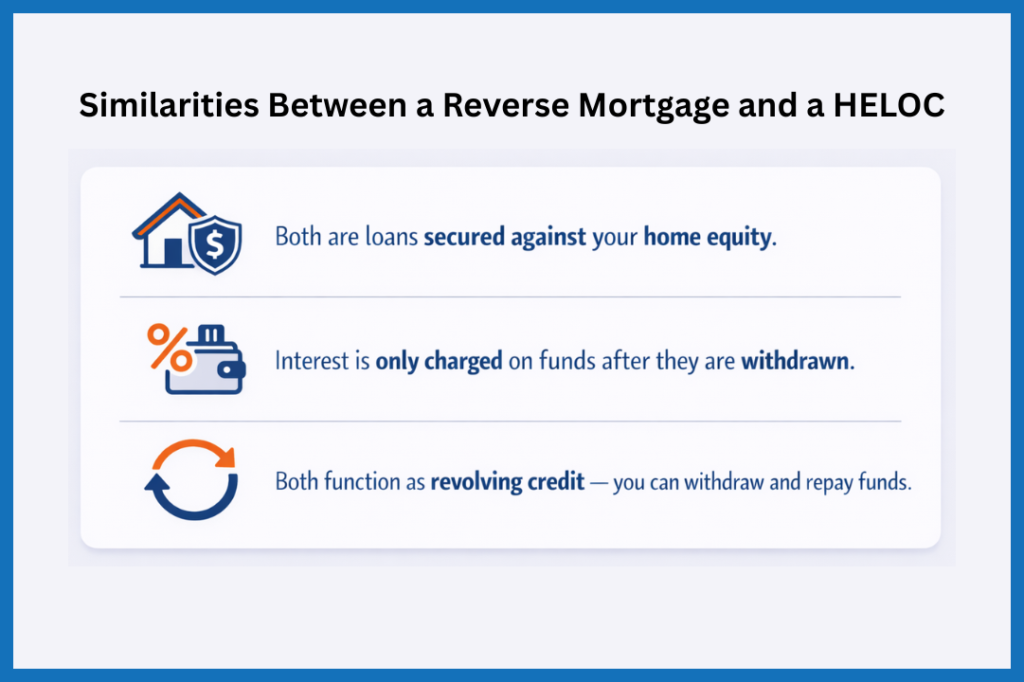

Reverse Mortgage vs. HELOC: How do the options compare?

When seniors do consider tapping into equity, they often weigh the HECM against the more familiar Home Equity Line of Credit (HELOC). The choice often comes down to the trade-off between monthly cash flow and equity preservation.

Feature | Reverse Mortgage (HECM) | Home Equity Line of Credit (HELOC) |

|---|---|---|

How it's paid back | Due when the last borrower leaves the home permanently. | Requires immediate, ongoing monthly payments of interest or principal. |

Who it's best for | Retirees with limited cash flow who need long-term funds without a monthly bill. | Borrowers with high income who need short-term funds for specific projects. |

Impact on Equity | Reduces home equity over time as interest is added to the loan balance. | Preserves equity more effectively if the principal is paid down regularly. |

Risk of Default | Primarily linked to failure to pay property taxes or insurance premiums. | Linked to the inability to make required monthly loan payments. |

How can families bridge the gap between history and finance?

Addressing the resistance to reverse mortgages requires a shift from talking about "loans" to talking about "choices." If a senior is struggling to pay for medical care or home modifications, the "legacy" they are preserving may actually be a burden of future care costs for their children.

Open dialogue between generations is essential. When children reassure their parents that their quality of life is more important than a future inheritance, the psychological barrier of the Great Depression can begin to fade. Financial literacy also plays a role; HUD-approved housing counseling is a mandatory requirement for reverse mortgages to ensures that seniors understand the obligations of the loan.

Ultimately, a reverse mortgage is a tool, not a trap. For those whose identities are tied to the debt-free safety of their home, it will always be a difficult sell. However, in the economic landscape of 2026, understanding the historical roots of that fear is the first step toward making a more informed, fear-free decision about the future.

Frequently Asked Questions

Can I lose my home if I take out a reverse mortgage?

You remain the owner of the home. However, you can face foreclosure if you fail to meet your obligations, which include paying property taxes, maintaining homeowners insurance, and keeping the home in good repair.

Does the bank own my house after I sign the paperwork?

No. This is a common myth. The bank or lender merely holds a lien against the property, similar to a traditional mortgage. Title and ownership stay with you as long as you live in the home and meet the loan requirements.

Will my children be stuck with the debt if the home value drops?

Most reverse mortgages are "non-recourse" loans. This means neither you nor your heirs will ever owe more than the home's market value at the time of sale, even if the loan balance has grown to exceed that amount. Any remaining equity after the loan is paid off belongs to your estate.

Discussion