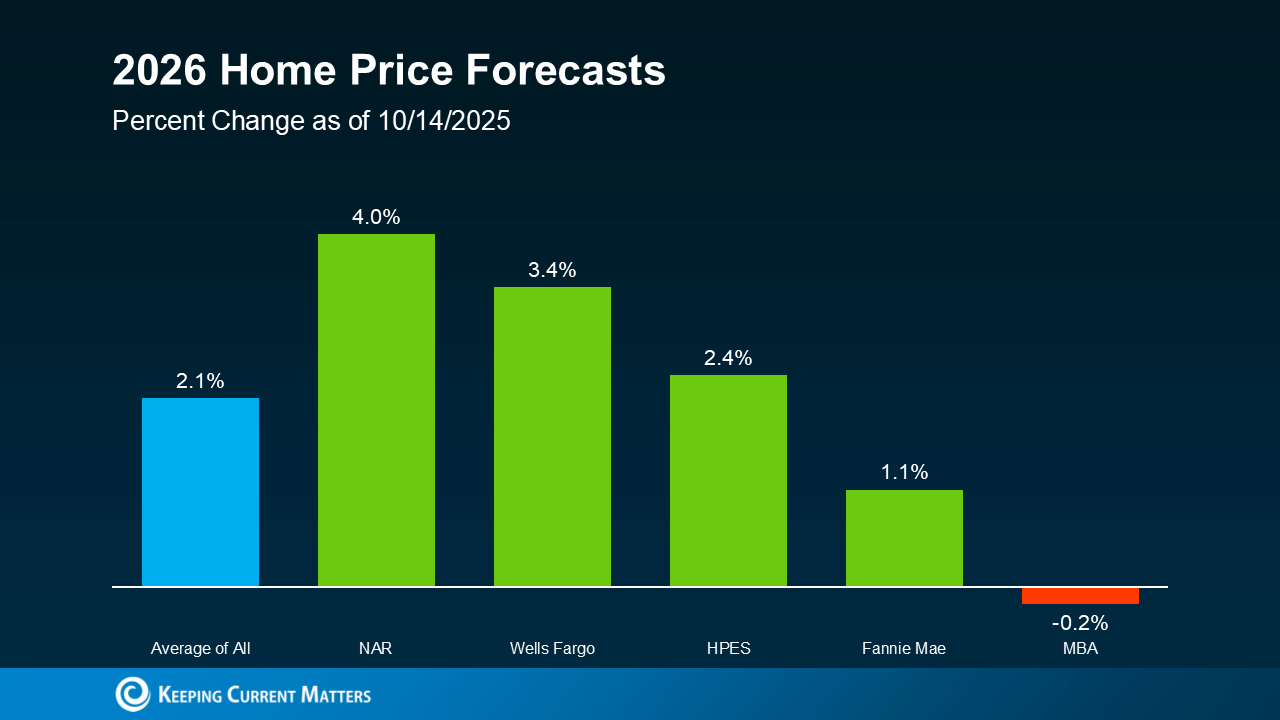

Buying a home in 2026 requires a strategy built on stability rather than the frantic competition of recent years. After a prolonged period of high rates and stagnant inventory, the market has transitioned into a more predictable "recovery phase" characterized by modest 2.2% price growth and a significant 9% increase in available inventory. For buyers, this shift means more selection and a return to traditional negotiation, provided they can navigate the plateauing interest rate environment.

As a mortgage broker, I see 2026 as the year of the "informed borrower." The Federal Reserve has signaled a steady hand, maintaining the federal funds rate in the 3.50%–3.75% range as of June 2026. This baseline has stabilized 30-year fixed mortgage rates, which are forecasted to average 6.3% through the remainder of the year. While these aren't the historic lows of the early 2020s, the predictability allows for more confident long-term financial planning.

How will the 2026 housing market impact your wallet?

The 2026 housing market is defined by a slow thaw in inventory and a deceleration in price appreciation. National forecasts suggest that for-sale inventory will continue to recover, climbing nearly 9% year-over-year, which finally offers buyers alternatives to the "take it or leave it" scenarios of the past. Annual price growth is expected to stay in the low single digits, hovering around 2.2%, a stark contrast to the 10-15% surges seen in previous cycles.

This stability is a double-edged sword. While it prevents buyers from being priced out overnight, it also means that home equity will build more slowly. Buyers in 2026 should view their purchase primarily as long-term shelter rather than a rapid wealth-building vehicle. According to NAR 2026 Forecast Summit data, this rising supply is expected to open up the market for those who have been sitting on the sidelines for the last three years.

What interest rate environment should you expect?

Mortgage rates in 2026 have moved away from the volatile spikes of 2024-2025, settling into a range that reflects the Federal Reserve's long-term "dot plot" projections. Current market assessments from Federal Reserve June 2026 reports suggest that the benchmark federal funds rate will likely persist in the low 3% range through the next two years.

For a home buyer, this translates to 30-year mortgage rates that are widely expected to move between 6.0% and 6.5%. While some regional variations exist, the national "middle road" has made the cost of borrowing easier to stomach for households with a strong income profile. However, it is important to remember that mortgage rates are not solely determined by the Fed; treasury yields and term premiums still play a vital role in daily rate fluctuations.

Metric | 2026 Forecast Value | Significance for Buyers |

|---|---|---|

Mortgage Rate Average | 6.3% | Establishes the baseline for monthly affordability and DTI calculations. |

Home Price Growth | +2.2% | Indicates a stable market where buyers are less likely to overpay. |

Inventory Growth | +9.0% | Provides more options, reducing the need for aggressive bidding wars. |

Existing Home Sales | 4.13 Million | Signals a moderate increase in market liquidity and moving options. |

Why does credit score matter more in 2026?

While you don't need a perfect 800 score, the "spread" between interest rates for good versus excellent credit has widened. In 2026, a credit score of 620 remains the general minimum for most conventional loan programs, but reaching the 740+ Tier is where the most significant savings are realized. Lenders continue to pull from all three major bureaus—TransUnion, Experian, and Equifax—and typically use the middle score of the borrower to determine the loan terms.

New flexibility in automated underwriting systems has helped first-time buyers, but the fundamental debt-to-income (DTI) requirements have remained strict. Most lenders are targeting a DTI of 43% or less, though some conventional and government-backed programs allow for DTI up to 50% if the borrower has "compensating factors" like high cash reserves (liquid assets) or a significant down payment.

Which loan programs offer the best entry points?

First-time homebuyers in 2026 are looking toward programs that prioritize low down payments to preserve cash for maintenance and renovations. The three main pathways for entry include:

Conventional 3% Down: Ideal for buyers with credit scores above 720. This allows for a low down payment while keeping private mortgage insurance (PMI) costs manageable.

FHA Loans: For those with credit scores as low as 580, FHA remains the gold standard, requiring only 3.5% down. It is particularly effective for those with higher existing debt but steady income.

Regional Bond Programs: Many states have launched 2026 initiatives that offer down payment assistance (DPA) to combat regional affordability hurdles, as noted in recent NAR outlook reports.

How are negotiations changing for buyers?

Negotiating power has tilted back toward buyers in 2026, marking a significant departure from the unconditional offers that dominated the previous five years. Buyers are no longer expected to waive critical protections like the inspection contingency or the appraisal gap contingency. In fact, a 2026 market update suggests that sellers are increasingly open to "concessions," which can reach up to 3% of the purchase price to help buyers cover closing costs or buy down their interest rates.

This "market flip" means your real estate agent should be focused on three key areas during the offer stage:

Seller-Paid Interest Rate Buydowns: Instead of asking for a price reduction, asking the seller to pay for a "2-1 buydown" can lower your mortgage rate by 2% in the first year, providing significant monthly relief.

Repair Credits: With inventory up 9%, buyers can once again insist on credit for old roofs, outdated electrical systems, or HVAC repairs identified during the inspection.

Extended Closing Timelines: Sellers who are also buyers are finding it easier to find their next home, meaning they are more flexible on closing dates than they were during the "moving crisis" of 2023.

Is new construction a viable alternative in 2026?

New residential construction has become a cornerstone of the 2026 market, with builders filling the gap left by homeowners who are still "locked in" to low 3% rates from the pandemic era. Major developers are offering aggressive financing incentives that often beat the national 6.3% average. It is common to see builder-affiliated lenders offering rates in the low 5% range for the first two years of a loan to stimulate sales.

However, buyers should weigh the location trade-offs. Most new developments are located in outlying suburban areas where land is more accessible. This can lead to longer commutes, though many companies in 2026 have finalized their long-term hybrid work policies, making a 45-minute drive more palatable if it only happens twice a week. When considering new construction, ensure you budget for "finishing costs" like landscaping, window treatments, and appliances, which are often not included in the base sticker price.

Understanding the "Lock-In" effect in 2026

The "lock-in" effect—where homeowners stay put to keep their extremely low mortgage rates—continues to influence the market, though its grip is loosening. As life events like weddings, births, and job changes accumulate, more of these residents are finally listing their homes. The Federal Reserve's decision to hold rates steady at 3.5% has created a psychological "new normal," convincing many would-be sellers that waiting for 3% rates to return is no longer a viable strategy.

This increase in listings is primarily seen in the mid-tier and luxury markets, while entry-level homes remain the most competitive segment. For the first-time buyer, this means that even though overall inventory has grown by nearly 10%, the "starter home" remains a prize that requires a strong pre-approval and a quick decision. Working with a mortgage broker who can explain these nuances is the best way to ensure you don't overextend yourself while trying to capture one of these elusive entry-level properties.

How should you prepare your finances for a 2026 purchase?

Preparation in 2026 should focus on "debt-clearing" rather than just "savings-growing." Because rates have stabilized at a higher plateau than in previous decades, your monthly debt obligations have a larger impact on your qualifying power. Every $100 monthly car payment or credit card bill can reduce your potential mortgage amount by nearly $15,000 in today's interest rate environment.

The best way to lower your DTI is to pay off revolving credit cards and avoid taking on any new installment loans (like auto financing) in the twelve months leading up to your home search. For those in Bellevue, WA, and other competitive markets, having a "fully underwritten pre-approval"—where a human underwriter has already reviewed your tax returns and pay stubs—is the key to moving quickly when the right property hits the market.

Frequently Asked Questions

Is 2026 a good time to buy a home? Yes, if you plan to stay for 5-7 years. The market is more stable than it has been in years, with inventory growing by 9% and price increases slowing to a manageable 2.2%. This provides a less stressful environment for careful selection and inspection.

What is the minimum credit score for a mortgage in 2026? While you can qualify for an FHA loan with a 580 score, most conventional lenders prefer 620 or higher. To get the best rates (closest to the 6.3% national average), you should aim for a score at or above 740.

How does debt-to-income (DTI) affect my buying power? Lenders generally want your total monthly debt payments (including the new mortgage) to be 43% or less of your gross monthly income. In 2026, keeping this ratio low is essential because higher interest rates naturally consume more of that percentage than they did in the past.

Will home prices drop in 2027? Most experts, including those from Realtor.com and NAR, forecast a stable market rather than a crash. Current indicators point toward modest price appreciation continuing rather than a sharp decline, thanks to the gradual nature of the inventory recovery.

Buying a home today is about patience and preparation. By understanding the 2026 landscape—stabilizing rates, growing inventory, and strict but fair lending standards—you can move from being a hopeful searcher to a successful homeowner.

Discussion